Millions of Americans are bracing for what experts call a looming “coverage cliff.” The Kaiser Family Foundation estimates that over 15 million people could lose affordable insurance by 2026 without congressional renewal of enhanced tax credits.

For many families, the question isn’t whether premiums will rise, but whether they’ll still have coverage when the safety net unravels.

A Slow Undoing of Rural Gains

Health officials warn that the impact could be devastating in rural states, where coverage gains took years to build. Idaho Health Exchange CEO Pat Kelly said, “Enhanced tax credits have strengthened communities.” Without this coverage, small-town hospitals may lose their financial footing.

The rollback jeopardizes economic development for hardworking families nationwide. For many, this isn’t just about policy but survival.

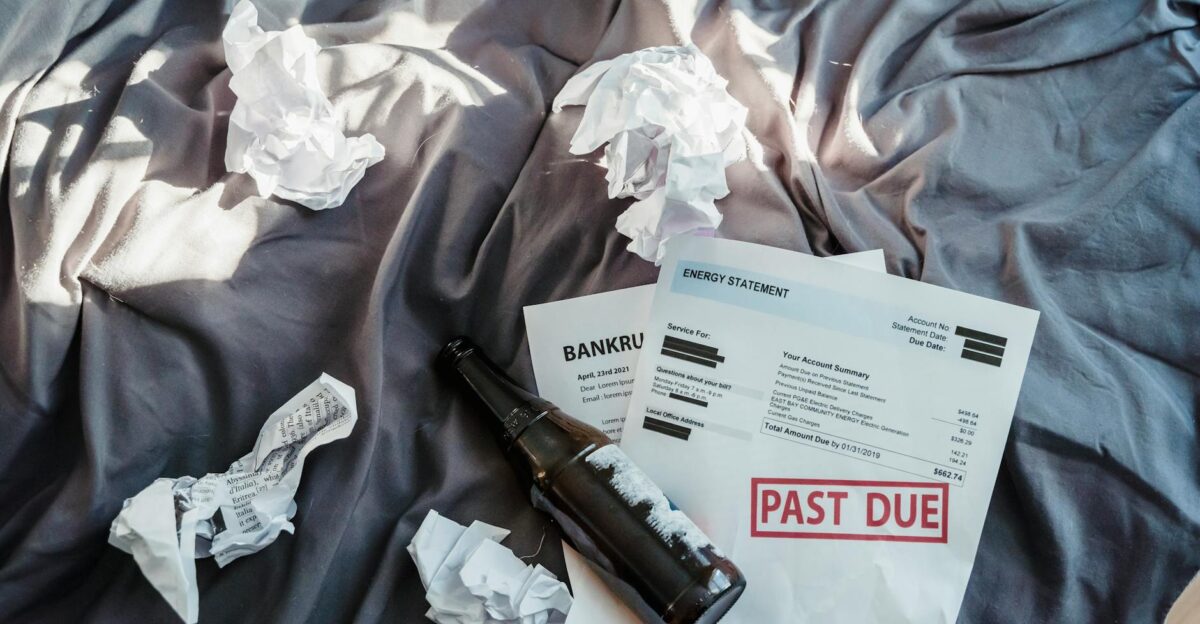

Premiums Poised to Soar

According to Kaiser Family Foundation data, Marketplace premiums could jump by more than 100% once subsidies expire. North Dakota Insurance Commissioner Jon Godfread told reporters that some families paying $800 a month could soon face bills of $3,000.

Insurers warn that the math is simple: fewer subsidies mean fewer enrollees, and fewer enrollees mean higher prices for everyone else.

The Return of the Uninsured

The uninsured rate, which hit historic lows in 2023, is now climbing again. According to NPR reporting, in parts of South Texas, one in three people already lacks coverage.

Health law expert Sara Rosenbaum of George Washington University said the loss of enhanced subsidies could leave many priced out of insurance, even if they technically qualify. The erosion threatens to undo a decade of progress.

Congress in a Stalemate

On Capitol Hill, lawmakers remain deeply divided. Supporters of renewal say the enhanced tax credits stabilized premiums and reduced medical debt. Critics argue they’re fiscally irresponsible.

One senator described the impasse as “a tug-of-war between compassion and cost.” As hearings drag on, state exchanges warn they need clarity soon or millions could face coverage lapses by early 2026.

Southern States Brace for Fallout

According to state insurance commissioners, Texas, Georgia, and Mississippi could see the steepest coverage declines. The Texas Tribune reports that up to 1.7 million Texans may lose coverage as subsidies lapse.

State health officials say rural and minority communities will be hit hardest, widening an already troubling healthcare gap. For many families, the loss feels less like policy and more like abandonment.

Medical Debt Creeps Back

Even with insurance, Americans carry more than $220 billion in unpaid medical bills, according to the Urban Institute. Without premium assistance, that number could rise sharply.

Patient advocates interviewed by NPR have described choosing between rent and life-sustaining medication. For many, the loss of affordable plans would turn every prescription into a financial gamble.

Hospitals at the Breaking Point

Hundreds of rural hospitals remain on the brink. USA Today reported that at least a dozen facilities in Nebraska and Kansas have closed since pandemic-era support ended. Health policy analysts warn that as coverage shrinks, hospital revenue follows.

The American Hospital Association cautions that more than 600 rural hospitals nationwide are now at risk of shutting their doors.

A Growing Divide

Coverage losses are expected to deepen racial and economic divides. Families USA, a nonpartisan advocacy group, noted that uninsured rates among Black and Hispanic adults could rise fastest.

When people lose coverage, costs shift to those who remain insured through higher premiums. “It’s not charity—it’s economics,” one Families USA analyst said. “Everyone pays when fewer people are covered.”

The Marketplace Tightens

Marketplace shoppers are already feeling the pressure. Cynthia Cox, vice president at the Kaiser Family Foundation, said consumers could face steep rate hikes that make insurance unaffordable for middle-income earners.

Insurers are reducing plan options and raising rates to offset uncertainty. As healthy enrollees drop out, risk pools shrink, driving prices higher—and pushing more families to the sidelines.

Red Tape and Work Rules Return

In several states, new Medicaid work-reporting rules are pushing people off the rolls. An Urban Institute report found that most who lost coverage were working but failed to submit the required paperwork. “Good, hardworking people will be shut out over technicalities,” researchers wrote.

One missed form can mean months without medical care for families juggling jobs, child care, and aging parents.

Millions Could Receive Termination Notices

State health agencies are quietly preparing for what they call “unintentional disenrollment.” Without federal renewal, millions could receive cancellation notices for ACA plans by mid-2026.

Health officials in Michigan and Ohio warn that even brief gaps in coverage can disrupt cancer treatments or vital prescriptions. The concern, as one policy expert put it, is “losing people in the paperwork.”

Insurers Raise Rates in Anticipation

Insurance companies are already building uncertainty into next year’s pricing. Early rate filings reviewed by KFF show proposed premium hikes averaging 17% nationwide.

One industry analyst said, “Insurers aren’t assuming Congress will act. They’re preparing for the worst.” That caution comes at a cost—borne by consumers who are already struggling to keep up with rising medical expenses.

A Fragile Economy Makes It Worse

If the economy falters, coverage losses could accelerate. During previous recessions, job cuts pushed millions onto public insurance, according to Health Affairs research.

Those safety nets may crumble without federal subsidies when families need them most. Economists warn that the combination of job loss and premium hikes could leave millions uninsured at the worst possible time.

Clinics Under Strain

Community clinics serving uninsured patients are also preparing for the fallout. Leaders at the National Association of Community Health Centers warn that as insurance coverage declines, clinic revenues will drop, forcing layoffs or reduced hours.

“We’re the last defense in rural healthcare,” a Montana clinic director said. “When we cut back, entire towns lose access to basic care.”

A Measurable Decline in Health

Studies published in JAMA Health Forum link insurance loss directly to worse health outcomes. When coverage lapses, people skip preventive care, delay prescriptions, and end up in emergency rooms once conditions worsen.

Public health experts say the trend is consistent: higher uninsured rates translate into higher mortality. Behind each data point are real lives and families affected.

Politics at the Core

The debate has become a political flashpoint. Hospital associations, governors, and advocacy groups are urging Congress to act, warning of a “national health coverage crisis.” While Democrats push for renewal, some Republican lawmakers demand offsets elsewhere in the budget.

As Forbes recently noted, even a short government funding lapse could trigger “crisis-level premium hikes and Medicaid losses.”

Families Forced to Choose

As prices rise, many households are cutting essentials to keep their coverage. NBC News reports that families in Michigan and Ohio are opting for higher deductibles and skipping checkups to save money.

One mother said, “We can’t afford to get sick.” For working families, the growing fear isn’t just about losing insurance—it’s about losing stability altogether.

Experts Urge a Long-Term Fix

Health economists argue that patchwork renewals are no substitute for reform. The Commonwealth Fund urged Congress to adopt a long-term stabilization plan, warning that “temporary fixes lead to recurring crises.”

Experts say that without structural change, the uninsured rate could climb by millions within a decade, pushing hospitals, states, and families back into the same vicious cycle.

The Clock Is Running Out

Congress has only weeks to decide whether to extend the subsidies or let them expire. Health leaders say the uncertainty alone is destabilizing the market.

“Every delay increases anxiety for families,” said Idaho exchange CEO Kelly. Behind every statistic is a person waiting—hoping lawmakers see more than numbers when they finally cast their votes.