The U.S. Small Business Administration has long prided itself as a steward of American entrepreneurship, approving $1.2 trillion in pandemic relief loans since 2020. Most arrived swiftly, with minimal scrutiny. But behind the scenes, federal auditors were noticing something troubling in Minnesota’s applications.

Red flags mounted quietly through 2025, and by late December, the SBA’s newly confirmed administrator had seen enough. What happened next would trigger the agency’s most aggressive enforcement action in recent history.

The Numbers Start Moving

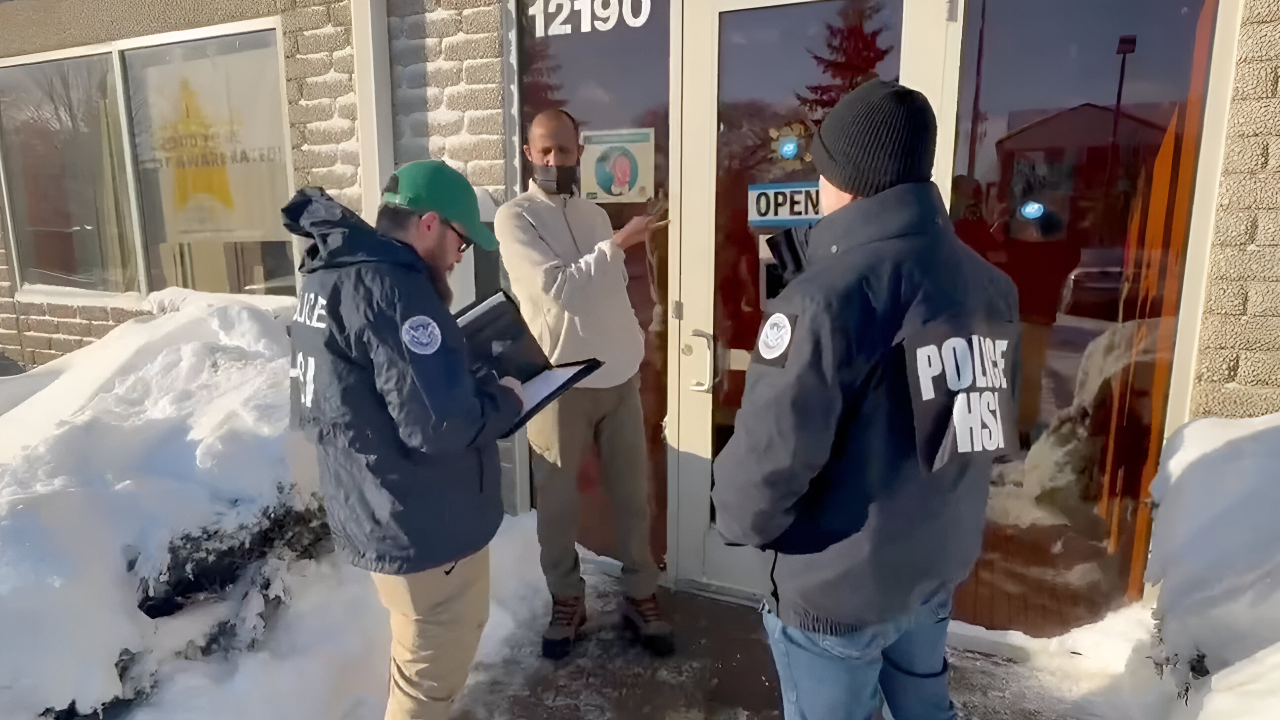

Fourteen months into Kelly Loeffler’s tenure as SBA Administrator, a former Georgia senator and fintech executive, her team initiated a sweeping week-long audit of pandemic-era loans across a single state. The scope shocked even seasoned federal investigators.

By the time the review concluded, 7,900 loans had been flagged. The borrower count was staggering: nearly 7,000 individuals suspended from all future SBA programs. And the dollar amount tied to suspected fraud? Approximately $400 million. The sheer concentration of alleged malfeasance in one state triggered an extraordinary response.

A Program Built for Speed, Vulnerable to Abuse

When President Trump signed the CARES Act on March 27, 2020, the Paycheck Protection Program (PPP) and Economic Injury Disaster Loan (EIDL) program were designed for speed. Get capital to struggling businesses fast. Forgiveness was built into PPP by design: meet certain payroll thresholds, and the loan vanishes. Between 2020 and 2021, over $800 billion in PPP funds were disbursed.

By mid-2023, roughly 92% had been forgiven. The SBA Office of Inspector General later estimated that approximately $200 billion, or about 17% of total disbursements, across both programs may have involved fraud. Minnesota’s emerging pattern suggested it concentrated far above the national average.

Minnesota’s Peculiar Vulnerability

Minnesota harbors the largest Somali-American diaspora in the United States, with over 65,000 residents of Somali descent concentrated primarily in Minneapolis. While the vast majority are law-abiding entrepreneurs, a subset has become infamous for social services fraud, starting around 2020.

The “Feeding Our Future” scheme alone defrauded the state’s Department of Human Services of an estimated $250 million. Now, federal auditors were discovering that the same networks or networks operating in parallel had penetrated pandemic loan programs. The patterns were eerily similar: shell companies, inflated applications, and rapid cash dispersal.

6,900 Minnesota Borrowers Banned Outright

On January 1, 2026, SBA Administrator Kelly Loeffler announced the agency’s most aggressive enforcement action in recent memory: the immediate suspension of 6,900 Minnesota borrowers from all SBA loan programs, including disaster assistance. These individuals were approved for 7,900 PPP and EIDL loans totaling approximately $400 million.

The action barred them permanently from accessing federal small-business capital. No state had ever faced such a concentrated ban. Loeffler’s statement was unambiguous: “Today, our agency took action to suspend 6,900 Minnesota borrowers amid suspected fraudulent activity.” The enforcement action marked a stark reversal from the approval-at-scale mentality that had defined the pandemic’s early months.

Immediate Impact in Minneapolis

The ripples were felt instantly in Minnesota’s business corridors. The 6,900 banned borrowers represented a mix of individuals and shell entities registered across the state. Minneapolis, St. Paul, and suburbs like Bloomington and Edina accounted for a disproportionate share. According to the Star Tribune analysis, the flagged loans represent roughly 5% of all PPP and EIDL loans approved in Minnesota during the pandemic period, suggesting that a far larger universe of legitimate borrowers existed.

Still, the concentration of fraud was startlingly high in discrete networks. Local lenders scrambled to understand exposure; some small business groups demanded clarity on whether the suspensions would affect future lending to legitimate borrowers in the Somali-American community.

Loeffler’s Call to Governor Walz

In a letter dated December 23, 2025, one week before the public announcement, Loeffler sent a stark message to Minnesota Governor Tim Walz. The SBA would immediately halt $5.5 million in annual federal support to Minnesota resource partners, including nonprofit agencies and community lenders, tasked with counseling and steering borrowers toward SBA programs.

The letter signaled that the SBA held state-level partners partially accountable for the fraud tsunami. Walz, a Democrat, found himself defending his administration’s oversight. The political pressure mounted swiftly. Loeffler’s move suggested the fraud extended beyond individual borrowers to implicate the systems and gatekeepers that approved them.

The Somali Network Thread

Federal law enforcement had already been investigating overlapping fraud schemes within segments of Minnesota’s Somali-American community. By September 2025, the U.S. Attorney’s Office had indicted eight individuals on charges related to Minnesota’s social services fraud scandal. At least six were members of the Somali community, according to prosecutors. Now, a related pattern emerged in pandemic lending.

Court documents and law enforcement sources indicate that at least $2.5 million in PPP and EIDL funds was connected to schemes operated by individuals also under investigation for theft of social services. The networks appeared to operate with alarming sophistication, filing applications across multiple program channels simultaneously.

Scope Dwarfs Previous Enforcement Actions

Before the Minnesota ban, the SBA had conducted numerous investigations into fraud. A mid-2000s case involving roughly 76 fraudulent 7(a) loans totaling $76 million had been considered a landmark enforcement action. The Minnesota case, involving 6,900 borrowers and $400 million, represented an order-of-magnitude increase.

SBA and Department of Justice press releases began using terms like “staggering,” “unprecedented,” and “the first state targeted in a comprehensive fraud crackdown.” Federal prosecutors signaled that additional state-level audits were imminent. Loeffler herself told the public: “This is just the first state,” implying that what Minnesota faced was an opening salvo in a nationwide enforcement wave.

$430M More in Flagged but Funded PPP

In her letter to Governor Walz, Loeffler concealed a secondary revelation: an additional $430 million in PPP funds, tied to approximately 13,000 loans, had been flagged as “potentially fraudulent” during the same review period. However, these loans had already been funded and, in many cases, forgiven. Some had been forgiven during the Biden administration.

Taxpayer money was already lost. Unlike the 6,900 borrowers who faced suspension, these loans had slipped through with minimal consequence. The disclosure raised a thorny question: If the SBA’s review identified fraud in these 13,000 loans, why were they funded and subsequently forgiven? Were there gaps in underwriting, or had fraud detection simply lagged?

Frustration in the Federal Ranks

Behind the scenes, federal auditors and FBI agents working pandemic loan fraud cases expressed mounting frustration. One law enforcement official quoted anonymously in December 2025 interviews described the pace of fraud discovery as “outpacing remediation.” SBA investigators had flagged thousands of loans for months; approval processes had moved far faster.

Internally, there was tension between those demanding swift public action and those arguing that premature disclosure could compromise ongoing investigations. Loeffler’s announcements settled the debate: get ahead of the narrative, suspend borrowers, and signal zero tolerance. But veteran investigators warned that suspensions alone wouldn’t recover stolen funds.

Leadership Shift and Mandate Change

Loeffler’s aggressive stance reflected a sharp pivot in SBA leadership philosophy. Her predecessor under the Biden administration had focused on expanding access to lending, especially in underserved communities.

Loeffler, by contrast, arrived with an explicit mandate from President Trump to “address waste, fraud, and regulatory overreach.” Her business background, as the former CEO of fintech firm Bakkt, and her 25 years in financial services meant she understood both loan mechanics and fraud schemes. Within weeks of taking office, she initiated a comprehensive review of Minnesota. Some observers credited her for swift action; critics argued the sweep was too blunt, potentially harming legitimate borrowers in affected communities.

The Recovery Question: Can Anyone Pay It Back?

As suspension orders were issued on January 1, 2026, a more pressing question emerged: recovering the $400 million. The SBA had tools such as asset seizures, salary garnishments, and civil False Claims Act suits. As of April 2024, law enforcement had recovered over $8 billion in EIDL funds returned by institutions and $20 billion by borrowers across all programs.

But that recovery rate reflected a massive national fraud pool ($200 billion) and took years. In Minnesota, many suspects were judgment-proof: they’d dispersed cash rapidly, purchased luxury vehicles and real estate, or moved funds through informal money-transfer networks (known as hawalas) to Somalia. Recovery was possible but uncertain.

Criminal Prosecution Pipeline Expands

The Department of Justice signaled that it would pursue criminal charges against key figures in the Minnesota fraud networks. Loeffler’s announcement explicitly stated that “cases will be referred to federal law enforcement for prosecution and repayment.” As of early January 2026, the U.S. Attorney’s Office for Minnesota was preparing a multi-tranche indictment strategy.

The statute of limitations for pandemic fraud had been extended to 10 years under legislation signed by President Biden in August 2022, so investigators had ample time. Federal prosecutors estimated it could take 18–24 months to bring the most significant cases to trial. In parallel, civil recovery suits using the False Claims Act were being prepared.

What Comes Next? A National Reckoning Looms

Loeffler’s declaration that “this is just the first state” ignited speculation about which states would face similar scrutiny. California, Texas, Florida, and New York all distributed large volumes of pandemic loans. Preliminary SBA reviews suggested potential fraud concentrations in Texas and California, although no public bans had been announced.

The question hanging over Washington was whether Minnesota would catalyze a nationwide enforcement wave or remain an outlier. Industry observers warned that aggressive suspensions could create unintended consequences: legitimate small businesses in affected geographic areas might face lender hesitation, and entire communities could experience reduced access to federal capital during future emergencies.

The Political Reckoning in Minnesota

Governor Tim Walz faced immediate political blowback. Republicans seized on the fraud scandal as evidence of Democratic mismanagement; Walz countered that the schemes predated his administration and crossed party lines. However, the optics were damaging: Minnesota’s reputation for good governance suffered a setback.

The state’s broader social services fraud scandal involving billions in Medicaid fraud tied to the same Somali networks compounded the damage. Conservative commentators drew parallels between weak state oversight and the approval of pandemic loans. Democratic leaders in Minneapolis and St. Paul scrambled to distinguish between the state’s legitimate Somali-American business community and the criminal networks exploiting programs. The political fallout extended beyond state lines.

Global Dimensions: The Hawala Network

Investigators uncovered evidence that money from fraudulent pandemic loans had flowed through informal money-transfer networks (hawalas) to Somalia, where it fed remittance economies and, by some federal accounts, supported designated terrorist organizations. City Journal reported that law enforcement sources confirmed millions of dollars in stolen Minnesota state funds had been routed to Al-Shabaab, a designated terror group.

While no direct link between specific PPP/EIDL theft and terrorist financing had been publicly confirmed as of January 2026, the patterns raised national security implications that extended the scandal beyond simple fraud into geopolitical territory.

The Underwriting Failure: Systemic or Individual?

A critical question emerged: Was the fraud outbreak symptomatic of systemic SBA underwriting failures, or did it reflect deliberate criminal schemes that exploited programs designed for speed? SBA documents released in January 2026 suggested both factors. Some lenders had implemented inadequate controls for fraud detection. Others had processed applications with minimal vetting.

The SBA’s own approval processes had prioritized speed over scrutiny during the pandemic emergency. Yet sophisticated fraudsters had also deliberately filed false documents, fabricated payroll records, and misled lenders. The inquiry would determine whether systemic reform was needed, including tighter controls, slower processing, enhanced verification, or whether the issue was criminal sophistication outpacing reasonable oversight.

A Generational Shift in Fraud Risk Perception

The Minnesota scandal triggered a broader recalibration in how federal agencies perceived pandemic-era relief programs. For two years, the narrative had centered on program success: trillions disbursed, millions of jobs preserved, economic stability maintained. The revelation of potential fraud, with 17% of funds potentially disbursed fraudulently, and Minnesota’s concentration suggesting even higher local rates, inverted that narrative.

Congress began reconsidering emergency lending authority; budgets for SBA fraud detection units received increased appropriations. The scandal served as a cautionary tale about the costs of rapid-response governance: speed and fraud containment are inherently in tension. Future emergency programs would need to embed fraud detection from the outset, rather than adding it retroactively.

The Lasting Question: When Opportunity Becomes Theft

The Minnesota SBA ban ultimately crystallizes a fundamental question about government relief programs: How do you design emergency lending that reaches those who need it most while preventing exploitation by those who don’t? The answer remains elusive. The $400 million in suspected fraud tied to 6,900 Minnesota borrowers represents not only theft of taxpayer money but also a betrayal of the program’s intent to sustain legitimate businesses through crisis.

Loeffler’s swift action sent a message about accountability. However, the honest reckoning, involving criminal convictions, fund recovery, systemic reform, and the prevention of future schemes, will unfold over the years. For now, Minnesota stands as a cautionary marker: where emergency generosity meets sophisticated fraud, federal enforcement eventually arrives. The question is whether it comes too late.

Sources

CBS News Minnesota – SBA suspends thousands of pandemic-era loan borrowers approved by Minnesota over potential fraud

Fox News – SBA suspends nearly 7,000 Minnesota borrowers over suspected $400M pandemic loan fraud

Minneapolis Star Tribune – What we know about claims of SBA fraud in Minnesota as suspensions announced

City Journal – Minnesota Welfare Fraud: Some Funds Went to Al-Shabaab

New York Times – How Fraud Swamped Minnesota’s Social Services System

U.S. Small Business Administration – Kelly Loeffler Profile and SBA Office of Inspector General Reports